Healthcare is in a tricky state—that’s no secret. It’s getting harder and harder to maintain control over medical expenses, and cutting down on those costs is an absolute necessity for most. One answer employers are exploring? Reference-based pricing (RBP).

An alternative to traditional healthcare pricing, RBP caps the cost of services at a set “reference” amount. Instead of negotiating individual prices for each service, RBP sets price limits based on a reference, such as Medicare’s rates. The plan then pays a specific percentage above what they would otherwise be reimbursed. RBP aims to control costs by eliminating large variations in pricing across different providers for the same procedure, allowing for cost savings, increased transparency, and no out-of-network fees.

But does it hold up in action? It certainly has for one of BRMS’ clients, an agricultural company located in California.

The company had been considering an open-access reference-based priced medical plan with their brokerage for years, carefully analyzing the potential the plan had to augment benefits while simultaneously reducing the company’s costs. With three hundred employees to look out for, the company needed a way to provide for them without breaking the bank.

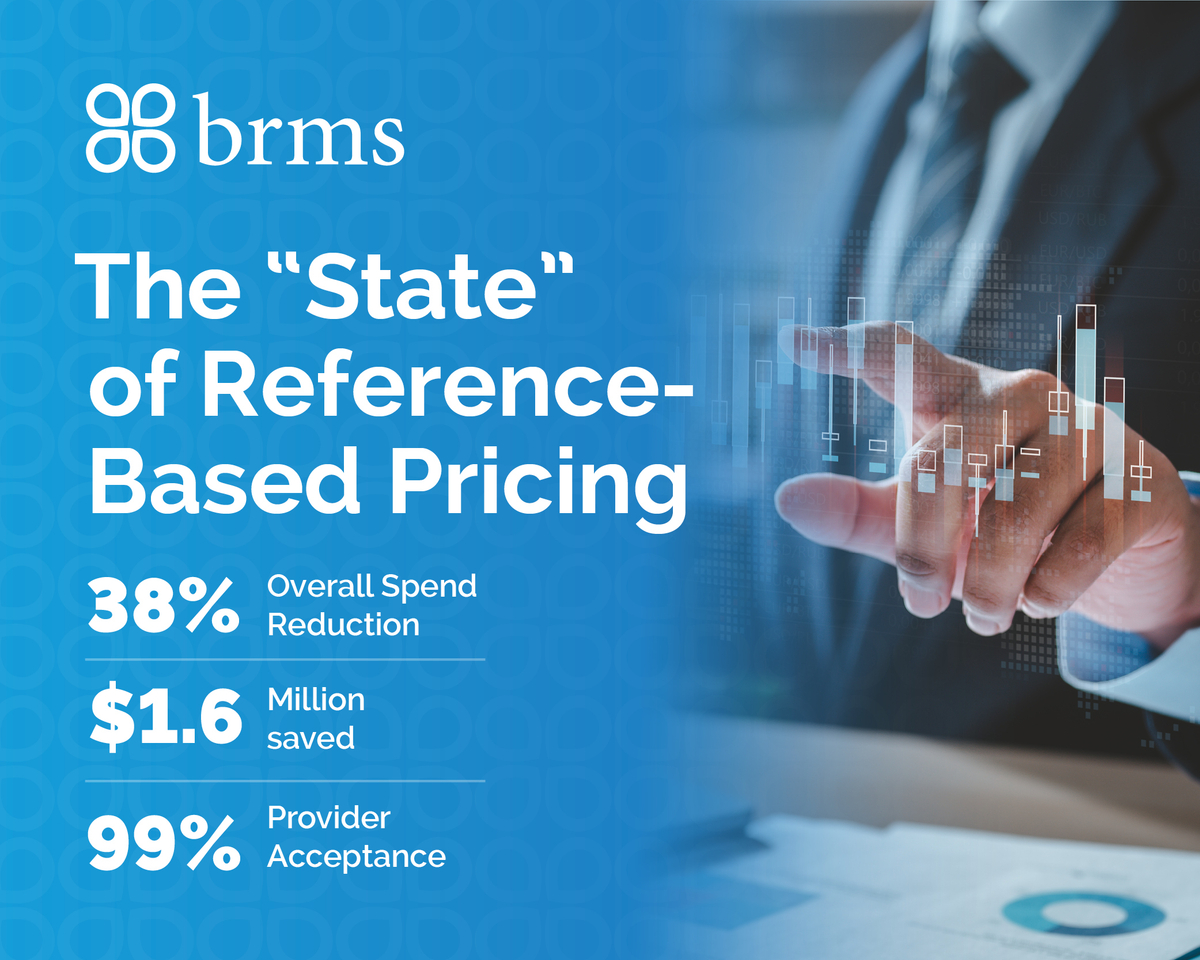

The relationship seemed to be an ideal fit—and the company employer quickly found it paid off, too. The RBP plan offered significant financial relief, without compromising the quality of the medical plan. By the end of year one, the numbers clearly showed the plan’s success—with a 38% overall spend reduction, $1.6 million saved, and a 99% provider acceptance. The transition to the new medical plan hadn’t just paid off; it had reduced office visit and hospital admission copays as well, improving employee health by a long shot.

Ultimately, there were only three provider-access issues during the entire year, all three of which were resolved, with proper care quickly delivered. After that first year, the company’s stop-loss renewed at a negative 10.1%. Claims per employee per month dropped from an average of $819 over the previous three years to $480—a 41.4% reduction. And, out of over 2,000 claims that were processed that year, zero known balanced bills were received.

RBP presents a significant opportunity for employers to tackle rising healthcare costs. In fact, the American Academy of Actuaries estimates that RBP could save up to 28% of service costs1. Of course, it’s important to keep in mind that every state is different—what works great in California might not work quite as well in, say, Alabama. But it’s undeniable that RBP poses a potential solution for rising healthcare prices—and a way to set price limits that brings a bit more fairness to the healthcare system.

Sources